Chief Economist Scott Brown discusses current economic conditions.

The Federal Reserve’s views on the economy and monetary policy are often of fine gradation, leading to misquotes, misinterpretations, and misunderstandings. The April 27-28 FOMC minutes are a good example.

Officials recognized that base effects (a rebound in prices that were depressed a year ago) would boost inflation in the near term:

“Participants also noted that the expected surge in demand as the economy reopens further, along with some transitory supply chain bottlenecks, would contribute to PCE price inflation temporarily running somewhat above 2%.

What does the Fed mean by “transitory?” It is not a defined time period. It could be a few months, or perhaps a lot longer, but it doesn’t mean permanent. The U.S. has experienced many input price spikes over the last few decades, none of which have contributed to an increase in the underlying inflation rate. Supply chain bottlenecks will ease over time. What’s different this time is the magnitude, boosted by unexpectedly strong demand. Vaccines have arrived and been distributed sooner than anticipated, fiscal stimulus has been larger than was projected at the start of the year, and the nature of the pandemic (weakness in consumer services) has boosted demand for consumer goods far beyond pre-pandemic levels. As a consequence, input price pressure are more pronounced than usual. According to the FOMC minutes, “a number of participants remarked that supply chain bottlenecks and input shortages may not be resolved quickly and, if so, these factors could put upward pressure on prices beyond this year.”

Fiscal policy will remain supportive, but less so over time, becoming a headwind to GDP growth into 2022 (although offset by an expected rebound in consumer services). The increase in household savings built up over the last year will be reduced over time. The pandemic is still a restraint in the near term, but supply chains should improve over time.

Much was made of the comments about asset purchases:

“In their discussion of the Federal Reserve’s asset purchases, various participants noted that it would likely be some time until the economy had made substantial further progress toward the Committee’s maximum-employment and price-stability goals relative to the conditions prevailing in December 2020, when the Committee first provided its guidance for asset purchases. Consistent with the Committee’s outcome-based guidance, purchases would continue at least at the current pace until that time. Many participants highlighted the importance of the Committee clearly communicating its assessment of progress toward its longer-run goals well in advance of the time when it could be judged substantial enough to warrant a change in the pace of asset purchases. The timing of such communications would depend on the evolution of the economy and the pace of progress toward the Committee’s goals. A number of participants suggested that if the economy continued to make rapid progress toward the Committee’s goals, it might be appropriate at some point in upcoming meetings to begin discussing a plan for adjusting the pace of asset purchases.”

Let’s deconstruct this paragraph. The FOMC has an outcome-based guidance, meaning that it needs to see “substantial further progress” towards in employment and inflation goals before reducing the monthly pace of asset purchases. “Substantial further progress” isn’t defined precisely, but as noted in the minutes, “participants generally noted that the economy remained far from the Committee’s maximum-employment and price- stability goals.” So, there is still a long way to go and the FOMC isn’t going to taper the pace of asset purchases until it gets there.

The last line of the paragraph is particularly nuanced. Now, it’s always the case that some Fed officials are more hawkish than others (meaning that, regardless of the circumstances, they would rather see monetary policy tightened sooner rather than later). The hawks are a small minority of senior Fed officials. “A number of participants” is more than a few, but less than several. The last line of the paragraph is far from a majority opinion. The phrase “It might be appropriate at some point” is not a solid conviction. As Fed Chair Powell has previously noted, the FOMC will discuss tapering the pace of asset purchase before actually tapering and will let the financial markets know when that discussion has begun.

Since the April FOMC meeting, input cost pressures appear to have increased further and some measures of inflation expectations have picked up. The key is whether we’ll see a sustained increase in inflation expectations, which we probably won’t.

Recent Economic Data

In the April 27-28 FOMC minutes, Fed officials noted that the central bank was a long way from achieving its employment and inflation goals and would wait for confirming data. “A number of participants suggested that if the economy continued to make rapid progress toward the Committee’s goals, it might be appropriate at some point in upcoming meetings to begin discussing a plan for adjusting the pace of asset purchases.”

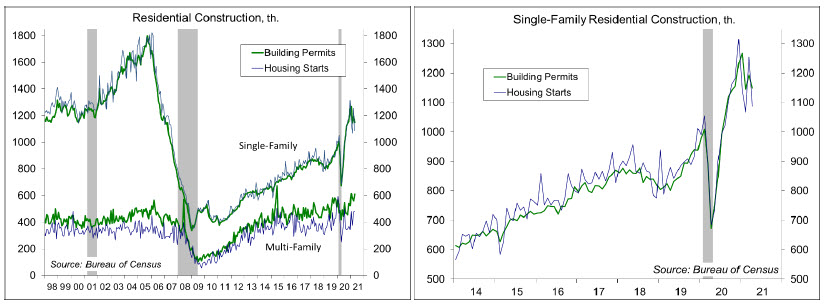

Building permits rose 0.3% in April (+60.9% y/y), reflecting some softness in the single-family sector and the usual noise in the multi-family sector. Housing starts fell 9.5% (+67.3% y/y).

Single-family building permits, the key figure in the report, fell 3.8% (+70.7% y/y), down across the four regions (-2.6% in the Northeast, -9.2% in the Midwest, -1.4% in the South, and -6.4% in the West).

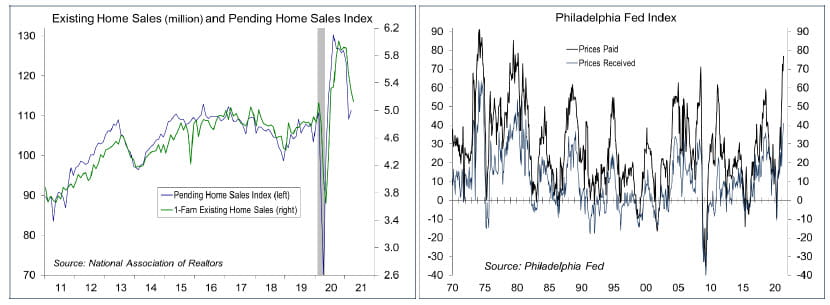

Existing home sales fell 2.7% in April, to a 5.85 million seasonally adjusted annual rate (+33.9% y/y). The National Association of Realtors cited a limited number of homes for sale.

The Philadelphia Fed’s monthly Manufacturing Business Outlook includes surveys of prices paid and prices received by the region’s manufacturers. Both indices are at their highest since 1980. However, these indices have spiked several times in the last few decades, without an increase in the underlying inflation trend.

The Conference Board’s Index of Leading Economic Indicators rose 1.6% in April (following +1.3% in July). Lower claims for unemployment benefits accounted for half the decline.

Gauging the Recovery

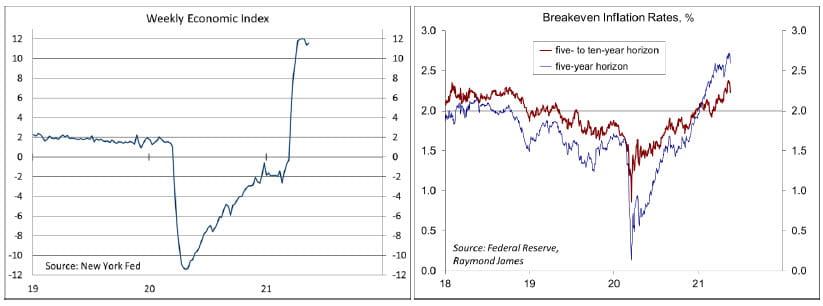

The New York Fed’s Weekly Economic Index edged up to +11.58% for the week ending May 15, up from

+11.36% a week earlier (revised from +11.45%), signifying strength relative to the weak data of a year ago. The WEI is scaled to year-over-year GDP growth (GDP was down 9.0% y/y in 2Q20).

Breakeven inflation (the spread between inflation-adjusted and fixed-rate Treasuries, not quite the same as inflation expectations) continues to suggest a moderately higher inflation outlook for the next five years. The 5-10-year outlook has crept above the Fed’s long-term goal of 2% (worth keeping an eye on).

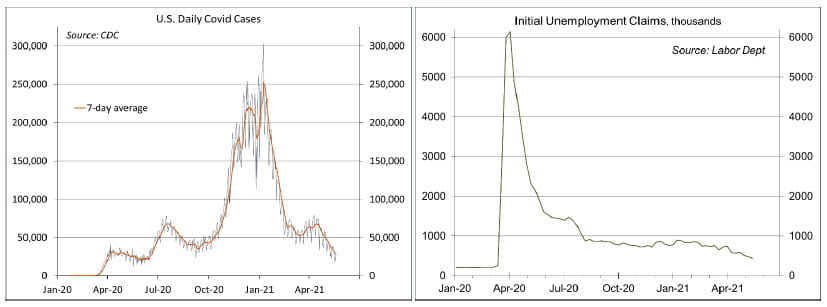

Not enough people are getting vaccinated, making it unlikely that the U.S. will reach herd immunity anytime soon, but the number of new cases is trending lower and restrictions are easing.

Jobless claims fell by 34,000, to 444,000 (another pandemic low), in the week ending May 15. Claims are trending lower, but are still well above pre-pandemic levels (a little over 200,000).

The University of Michigan’s Consumer Sentiment Index fell to 82.8 in the mid-month assessment for May (the survey covered April 28 to May 12), vs. 88.3 in April and 84.9 in March. The increase reflected growing concerns about inflation. The expected inflation rate for the next year rose to 4.6% (from 3.4% in April), while the expected rate for the next five years rose to 3.1% (from 2.7%). Two-thirds of those surveyed expect the Fed to raise short-term interest rates within a year.

The opinions offered by Dr. Brown are provided as of the date above and subject to change. For more information about this report – to discuss how this outlook may affect your personal situation and/or to learn how this insight may be incorporated into your investment strategy – please contact your financial advisor or use the convenient Office Locator to find our office(s) nearest you today.

This material is being provided for informational purposes only. Any information should not be deemed a recommendation to buy, hold or sell any security. Certain information has been obtained from third-party sources we consider reliable, but we do not guarantee that such information is accurate or complete. This report is not a complete description of the securities, markets, or developments referred to in this material and does not include all available data necessary for making an investment decision. Prior to making an investment decision, please consult with your financial advisor about your individual situation. Investing involves risk and you may incur a profit or loss regardless of strategy selected. There is no guarantee that the statements, opinions or forecasts provided herein will prove to be correct.

Markets & Investing Members of the Raymond James Investment Strategy Committee share their views on...

Markets & Investing Review the latest Weekly Headings by CIO Larry Adam. Key Takeaways ...

Technology & Innovation Learn about a few simple things you can do to protect your personal information...