Chief Economist Eugenio J. Alemán discusses current economic conditions.

The June consumer price index (CPI) report wasn’t what the doctors were recommending. But it wasn’t the top number, or headline inflation, that is moving markets and potentially the Fed. Everybody knew that oil and gasoline prices were going to have an outsized impact on the number and that was the reason for consensus expectations at 1.1% for the month. The problem was that the core consumer price index (Core CPI) was up by 0.7% versus 0.6% in May. And this means that not only are energy and food prices moving higher, but also the rest of the sectors of the US economy, with commodities (excluding food and energy commodities) prices increasing by 0.8%, new vehicles prices increasing 0.7%, used cars and trucks prices surging 1.6% once again, apparel prices increasing 0.8%, shelter prices up 0.6%, transportation services prices surging 2.1% and medical care services prices increasing 0.7%.

Thus, after the very negative CPI report the markets’ knee-jerk reaction was to price in an 80.3% chance that the Federal Reserve (Fed) would increase the federal funds rate by 100 basis points (100 basis points equals 1%) during the Federal Open Market Committee (FOMC) meeting to be held on July 26-27. If this is what happens during the FOMC meeting, then the federal funds rate will be slightly above what economists today consider the neutral federal funds rate.

That is, if the Fed goes with an increase of 100 bps during the July meeting, the federal funds rate will be at 2.50% to 2.75% in July, which is borderline restrictive if we assume that the neutral federal funds rate is about 2.25% to 2.50%.

However, two days after the CPI report (Friday July 15), markets have calmed down somewhat and now the bets are more even between a 75 basis point increase (53.6%) and a 100 basis point increase (46.4%). These odds will probably evolve over the next weeks before the FOMC meeting.

At this time we are inclined to say that the Fed is going to go for a 75 basis point hike because although retail sales were stronger than consensus, consumer demand was very weak in Q2. Meanwhile industrial production was also very weak at the end of the second quarter. So, the Fed will have lots of evidence to justify 75 basis points rather than 100 basis points. On top of this, five-year ahead inflationary expectations from the preliminary University of Michigan Index came in at 2.8%, which means that long-term inflation expectations remain anchored.

Inflation is Going to Slow Down

We know, and the Fed knows, that inflation is going to slow down in the near term because oil prices, and thus, gasoline prices, are down considerably in July compared to June. So, the top line CPI number is going to be lower in July compared to June. The year-on-year measure, on the other hand, is more difficult to predict, and will depend on what happens to core prices. If core prices continue to increase at current rates, the year-over-year rate may not come down too much depending on how strong the core rate is.

If the economy was in recession already, as many argue today, the Fed should not worry so much, as core prices are going to come down because American consumers will have no money to continue to buy these goods. But the economy is not in recession (even if second quarter GDP comes out negative) and if gasoline prices are coming down considerably in July, American consumers are going to spend less on gasoline but will probably use those savings to buy other goods and services, which could keep the core rate higher than what markets are expecting. However, as we said above, consumer demand has weakened considerably and thus will help keep prices contained in the coming months.

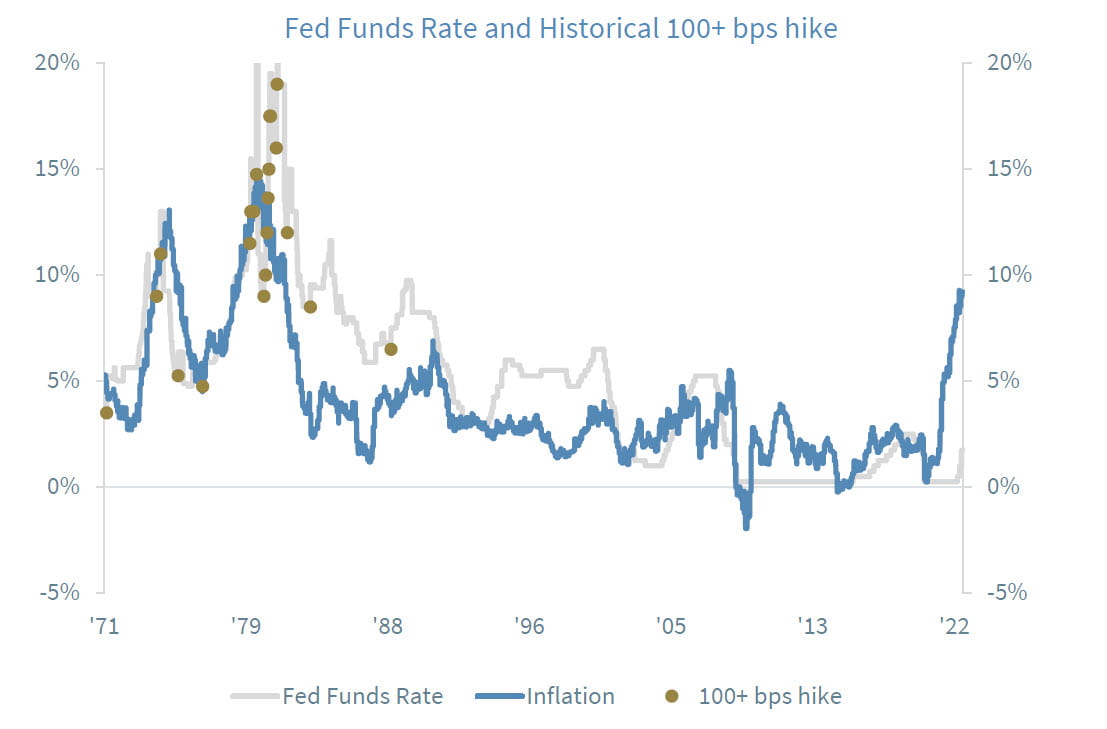

It Is Not The Fed’s First Rodeo

While the Fed increased the fed funds rate by 100 or more basis points 21 times between 1971 and 1988, the 75 basis point increase last month, and the potential (but not our call) 100 basis point increase later this month are unprecedented in size and scope. In fact, the last time the Fed raised the fed funds rate by

100 basis points was in 1988, when it raised it from 6.5% to 7.5%. However, that increase was approximately a 15% increase in the fed funds rate, while the 75 basis point increase last month was a record five times larger in percentage terms, as the Fed surprised markets and economists by increasing rates from 1% to 1.75%. Regardless of whether the number will be 75 or 100 basis points at the next meeting, the total increase in the last two months alone will still be close to a 150% increase in the federal funds rate.

The only other time in history that saw a triple digit increase in a short period of time was in the 1980s during the Volcker era. At that time, the federal funds rate increased from 9% in August of 1980 to 19.5% in December of that same year. However, the US economy back then was facing both high inflation and very slow growth, also known as ‘stagflation.’ Today, that’s not the case. While US inflation is at a 40-year high, the economy is slowing but still above potential output despite GDP numbers in Q1 and perhaps in Q2 suggesting otherwise.

Economic and market conditions are subject to change.

Opinions are those of Investment Strategy and not necessarily those Raymond James and are subject to change without notice the information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. There is no assurance any of the trends mentioned will continue or forecasts will occur last performance may not be indicative of future results.

Consumer Price Index is a measure of inflation compiled by the US Bureau of Labor Studies. Currencies investing are generally considered speculative because of the significant potential for investment loss. Their markets are likely to be volatile and there may be sharp price fluctuations even during periods when prices overall are rising.

Consumer Sentiment is a consumer confidence index published monthly by the University of Michigan. The index is normalized to have a value of 100 in the first quarter of 1966. Each month at least 500 telephone interviews are conducted of a contiguous United States sample.

The producer price index is a price index that measures the average changes in prices received by domestic producers for their output. Its importance is being undermined by the steady decline in manufactured goods as a share of spending.

Industrial production: Industrial and production engineering is a measure of output of the industrial sector of the economy. The industrial sector includes manufacturing, mining, and utilities.

Personal Consumption Expenditures Price Index (PCE): The PCE is a measure of the prices that people living in the United States, or those buying on their behalf, pay for goods and services. The change in the PCE price index is known for capturing inflation (or deflation) across a wide range of consumer expenses and reflecting changes in consumer behavior.

FHFA house price index is a quarterly index that measures average changes in housing prices based on sales or refinancing’s of single-family homes whose mortgages have been purchased or securitized by Fannie Mae or Freddie Mac.

Consumer confidence index is an economic indicator published by various organizations in several countries. In simple terms, increased consumer confidence indicates economic growth in which consumers are spending money, indicating higher consumption.

ISM Manufacturing indexes are economic indicators derived from monthly surveys of private sector companies.

ISM Services Index is an economic index based on surveys of more than 400 non-manufacturing (or services) firms’ purchasing and supply executives.

Non-Manufacturing Business Activity Index is a seasonally adjusted index released by the Institute for Supply Management measuring business activity and conditions in the United States service economy as part of the Non-Manufacturing ISM Report on Business.

New orders index measures the value of the orders received in the course of the month by French companies with over 20 employees in the manufacturing industries working on orders.

Source: FactSet, data as of 6/3/2022

Markets & Investing Members of the Raymond James Investment Strategy Committee share their views on...

Markets & Investing Review the latest Weekly Headings by CIO Larry Adam. Key Takeaways ...

Technology & Innovation Learn about a few simple things you can do to protect your personal information...