Read the weekly bond market commentary from Drew O’Neil

The yield that a bond is purchased at tells an investor what they will earn annually if the bond is held to maturity. The three “pieces” that work together to determine a yield are: the price of the bond, the cash flow the bond generates (coupon), and the maturity date. All three of these inputs are critical pieces of information needed to determine how much an investor could earn on the investment. Yet, it is not uncommon for investors to let the price of a bond be the determining factor as to whether a bond should be considered for purchase or not. These investors are making decisions based on an input into the equation, instead of analyzing the output. Price alone tells you nothing, whereas yield tells you everything.

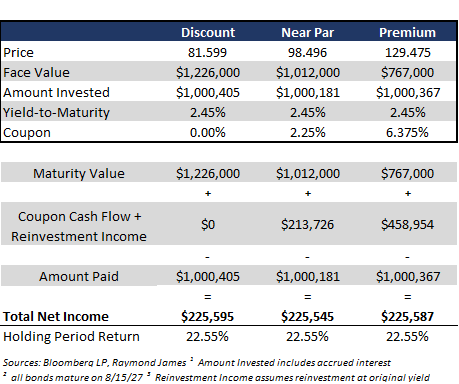

The chart below hopefully shines some light on this subject. Three bonds with identical maturity dates but with very different prices are compared. All of these bonds have a yield of 2.45%, meaning that an investor would earn 2.45% annually if they purchase any one of these positions. Knowing this, most investors should be indifferent as to which of these bonds is purchased, yet in reality, many would not even consider the bond priced at a large premium. In not even considering bonds priced at a premium, many investors are eliminating a large portion of the potential “buy candidates” right off the bat, limiting themselves to a small corner of the market and potentially missing out on valuable opportunities.

“Am I losing money if I buy a premium bond?”

You are not losing money if you buy a premium bond, you are earning whatever the yield on the bond is when you purchase it. If you were losing money, the yield would be negative.

The bottom two rows of this chart are what inpacts an investor’s wealth, yet many investors focus on the top row of the chart. The yield tells an investor what those bottom two numbers will be, not the price.

Benefits of Premium Bonds:

- High cash flow

- Lower duration than comparable lower coupon bonds

- Oftentimes, offer more yield than lower coupon comparable bonds due to many investors’ aversion to premium bonds (supply/demand)

- Larger selection of bonds, as given interest rate levels, a large portion of the market is currently priced at a premium

To learn more about the risks and rewards of investing in fixed income, please access the Securities Industry and Financial Markets Association’s “Learn More” section of investinginbonds.com, FINRA’s “Smart Bond Investing” section of finra.org, and the Municipal Securities Rulemaking Board’s (MSRB) Electronic Municipal Market Access System (EMMA) “Education Center” section of emma.msrb.org.

The author of this material is a Trader in the Fixed Income Department of Raymond James & Associates (RJA), and is not an Analyst. Any opinions expressed may differ from opinions expressed by other departments of RJA, including our Equity Research Department, and are subject to change without notice. The data and information contained herein was obtained from sources considered to be reliable, but RJA does not guarantee its accuracy and/or completeness. Neither the information nor any opinions expressed constitute a solicitation for the purchase or sale of any security referred to herein. This material may include analysis of sectors, securities and/or derivatives that RJA may have positions, long or short, held proprietarily. RJA or its affiliates may execute transactions which may not be consistent with the report’s conclusions. RJA may also have performed investment banking services for the issuers of such securities. Investors should discuss the risks inherent in bonds with their Raymond James Financial Advisor. Risks include, but are not limited to, changes in interest rates, liquidity, credit quality, volatility, and duration. Past performance is no assurance of future results.