Chief Economist Scott Brown discusses current economic conditions.

Brief summaries of key elements in the economic outlook.

The Big Picture: The overall economic outlook depends on the virus, efforts to contain it, and the degree of fiscal support. We’ve had a sharp- but-partial rebound in May and June, following a steep decline in March and April. The pace of improvement is expected to moderate. The impact of the pandemic has not been felt evenly. About 40% of those at the bottom 20% of income earners lost jobs in March and April, and a third to one half of those jobs have been recovered. Fiscal support has been a life line for unemployed workers. White collar workers have been more able to work from home. Mid- to upper-income spending has been curtailed by social distancing (the top 20% of income earners account for more than half of personal income and more than half of consumer spending).

Gross Domestic Product: There is enough improvement in May and June to suggest a record pace of GDP growth in 3Q20. The monthly-to- quarterly arithmetic may seem quirky, but quarterly growth often depends on the months leading into it. For example, if we were to see no monthly growth in July, August, and September, real consumer spending would still rise at a 26.8% annual rate in 3Q20. That’s 70% of GDP. Note that the advance estimate of 3Q20 GDP growth is set for October 29, just five days ahead of the November 3 election. Granted, a strong third quarter won’t take us back to the 4Q19 level of GDP, but it will easily be a record increase in quarterly GDP, which Trump will carry into the election (although it’s likely that many will vote early). The pace of GDP growth is expected to slow to a more moderate pace in 4Q20 and in 2021.

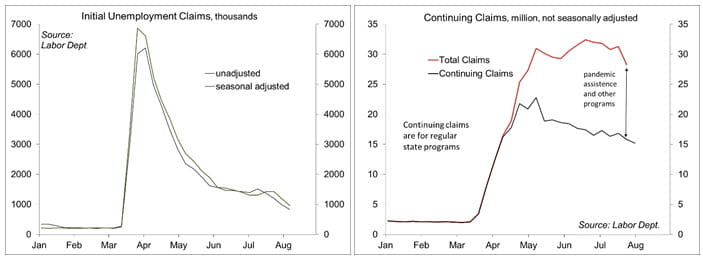

The Job Market: The reported unemployment rate has come down, to 10.2% in July, but that’s misleading. We’ve had some classification issues (furloughed workers counted as “employed,” rather than as “unemployed on temporary layoff”), but that was not as much of a problem as in April and May. More importantly, the reported unemployment rate always understates the weakness in a downturn, as many unemployed workers give up looking for a job and are no longer officially classified as “unemployed.” The labor force has declined over the last five months, but if it had kept on trend after February, the unemployment rate would now be around 13%. After 20 consecutive weeks at over one million, initial claims for unemployment benefits dipped below that level last week. The reported figure is exaggerated by the seasonal adjustment, which is multiplicative (unadjusted claims are at their seasonal lows in August and September). Unadjusted claims totaled 832,000 in the week ending August 8 – trending down, but still extremely high by historical standards.

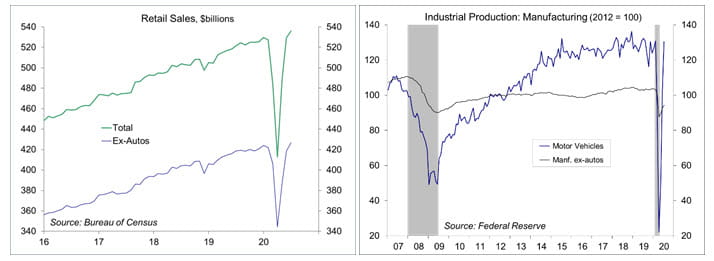

Consumer Spending: Retail sales continued to improve in July, and are now higher than they were in February (on a seasonally adjusted basis). However, the mix of spending is different and these changes are likely to be long lasting. Sales at apparel stores, department stores, and restaurants remain well below pre-pandemic levels. However, sales of motor vehicles, sporting goods, groceries, and home improvement goods have increased. Bear in mind that much of the pandemic weakness has been in consumer services, where we won’t see a full recovery until the pandemic is behind us.

Inflation: The Consumer Price Index has picked up in June and July, but that largely reflects a bounce-back in areas that had been depressed by the pandemic (apparel, transportation services, gasoline). Similar patterns are seen in the Producer Price Index and in import prices. Beyond the pandemic noise, there’s no sign of a higher underlying trend in inflation. The labor market is the widest channel for inflation pressures, and wage increases should be limited given the elevated unemployment rate. Large budget deficits and aggressive Fed policy are not going to be inflationary, and inflation is expected to track below the Fed’s target.

Federal Reserve Policy: A near-zero overnight lending rate and the expansion of the Fed’s balance sheet has no impact on the virus, but the Fed’s efforts have been focused on insuring adequate liquidity in the financial system.

Fiscal Support: Those hurt most by the downturn have been the least able to handle the loss of a job. Lower-income workers may make more through expanded unemployment benefits than they did working, but that’s not what’s preventing them from working – it’s the lack of jobs. There is plenty of anecdotal evidence of abuse. That happens in every downturn (for example, the surge in Social Security Disability in the recovery from the financial crisis), but support is critical for most lower-income workers. State and local budget pressures are building rapidly. Federal aid will be critical in preventing massive losses in state and local government jobs (we’ve already lost 1.17 million jobs, more than half in education). President Trump’s recent executive orders and promise to do away with payroll taxes are head-scratchers. The power to spend lies with Congress and payroll taxes fund Social Security (there is no “general fund” to make up the difference).

Recent Economic Data

The Consumer Price Index rose 0.6% in July (+1.0% y/y), also up 0.6% excluding food and energy (+1.6% y/y). The larger-than-expected increase in July reflected further rebounds in prices that were depressed due to extreme social distancing (apparel, transportation services, hotels, and gasoline) and similar rebounds from pandemic price declines were seen in the Producer Price Index and the report on import prices. Beyond the pandemic effects, underlying trends in inflation have remained low.

Retail sales rose 1.2% in July (+2.7% y/y), a little less than expected, but figures for June were revised higher. Auto dealership sales slipped 1.2% (up 4.0% from February and +6.1% y/y). Ex-autos, sales rose 1.9% (also +1.9% y/y). Core sales, which exclude motor vehicles, building materials, and gasoline, rose 2.0% (up 2.1% from February and +2.9% y/y). Total retail sales appear to have largely recovered, but the mix has shifted. Sales at department stores, apparel stores, and restaurants remain well below where they were in February, while sales of groceries, motor vehicles, sporting goods, home improvement supplies are all higher).

Industrial production rose 3.0% in the initial estimate for July (-8.2% y/y). The output of utilities rose 3.3% on warm weather (+0.6% y/y). Mining output rose 0.8% (-17.0% y/y), with oil and gas well drilling down 8.0% (-71.5% y/y) and energy extraction up 0.9% (-9.5% y/y). Manufacturing output rose 3.4% (-7.5% y/y), led by a 28.3% rise in motor vehicle production (-1.4% y/y). Ex-vehicles, factory output rose 1.6% (-8.2% y/y). Aerospace rose 7.5% (-20.5% y/y). Other sectors were mostly higher, but still below pre-pandemic levels.

Gauging the Recovery

Jobless claims fell to 963,000 in the week ending August 8, the first time below one million since mid-March. Seasonal adjustment is multiplicative and exaggerates the adjusted figure in August and September (when unadjusted claims are at their seasonal lows). Unadjusted claims fell to 832,000, still very high by historical standards. Continuing claims fell by 604,000 in the week ending August 1, to 15.486 million (that figure is for regular state unemployment insurance programs and does not include pandemic assistance and other programs). Total recipients, including all programs, were 28.258 million (not seasonally adjusted) for the week ending July 25 (down from 31.309 million in the previous week).

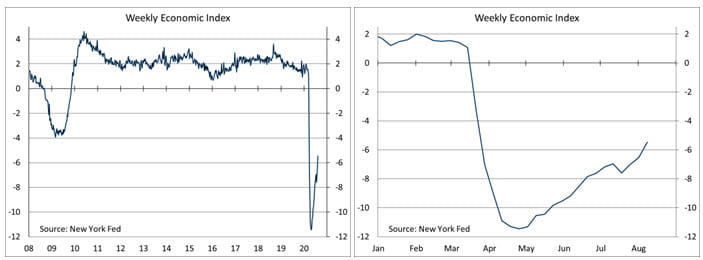

The New York Fed’s Weekly Economic Index rose to -5.47% for the week of August 8, up from -6.53% in the previous week and a low of -11.45% at the end of April. The WEI is scaled to four-quarter GDP growth (for example, if the WEI reads -2% and the current level of the WEI persists for an entire quarter, we would expect, on average, GDP that quarter to be 2% lower than a year previously).

The University of Michigan’s Consumer Sentiment Index was little changed at 72.8 in the mid-month assessment for August (the survey covered July 29 to August 12), vs. 72.5 in July and 78.1 in June. The report noted Two significant changes since April: consumers have become more pessimistic about the five-year economic outlook (-18 points) and more optimistic about buying conditions (+21).” The gridlock in Washington has undermined confidence in economic policies (the lowest since Trump first entered office) and “increased uncertainty and heightened the need for precautionary funds” as the school year gets underway.

The opinions offered by Dr. Brown should be considered a part of your overall decision-making process. For more information about this report – to discuss how this outlook may affect your personal situation and/or to learn how this insight may be incorporated into your investment strategy – please contact your financial advisor or use the convenient Office Locator to find our office(s) nearest you today.

All expressions of opinion reflect the judgment of the Research Department of Raymond James & Associates (RJA) at this date and are subject to change. Information has been obtained from sources considered reliable, but we do not guarantee that the foregoing report is accurate or complete. Other departments of RJA may have information which is not available to the Research Department about companies mentioned in this report. RJA or its affiliates may execute transactions in the securities mentioned in this report which may not be consistent with the report’s conclusions. RJA may perform investment banking or other services for, or solicit investment banking business from, any company mentioned in this report. For institutional clients of the European Economic Area (EEA): This document (and any attachments or exhibits hereto) is intended only for EEA Institutional Clients or others to whom it may lawfully be submitted. There is no assurance that any of the trends mentioned will continue in the future. Past performance is not indicative of future results.

Markets & Investing Members of the Raymond James Investment Strategy Committee share their views on...

Markets & Investing Review the latest Weekly Headings by CIO Larry Adam. Key Takeaways ...

Technology & Innovation Learn about a few simple things you can do to protect your personal information...