Chief Economist Scott Brown discusses current economic conditions.

There were no major surprises from the Fed policy meeting. The Federal Open Market Committee signaled that tapering would likely be announced in November, while Chair Powell indicated that it would likely come to an end around the middle of next year. While an increase in short-term interest is still a long way off, Fed officials generally brought forward their expectations for lift-off (officials were evenly split on whether that would start in 2022). Needless to say, while economic expectations have shifted, the level of uncertainty in the outlook is extremely high.

In its policy statement, the FOMC indicated that “if progress continues broadly as expected, the Committee judges that a moderation in the pace of asset purchases may soon be warranted.” In his press conference, Chair Powell suggested that the goal of “substantial further progress” in labor market conditions would likely be met in the October Employment Report. Barring any major economic surprises, we can expect a $15 billion reduction in the pace of asset purchases each month.

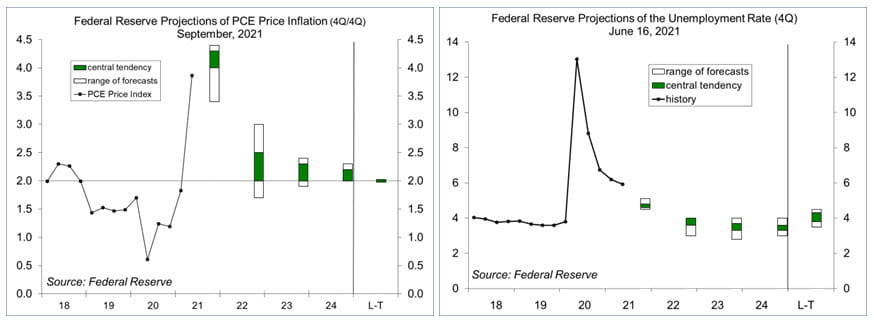

In the Summary of Economic Projections (SEP), senior Fed officials generally lowered their expectations for 2021 GDP growth (median now 5.9%, vs. 7.0% in June) and raised their outlook for 2022. The 2021 inflation was raised (4.2%, vs. 3.4% in June), but officials expect inflation to fall back to 2.2% in 2022 and 2023 (that is, higher inflation still expected to be transitory).

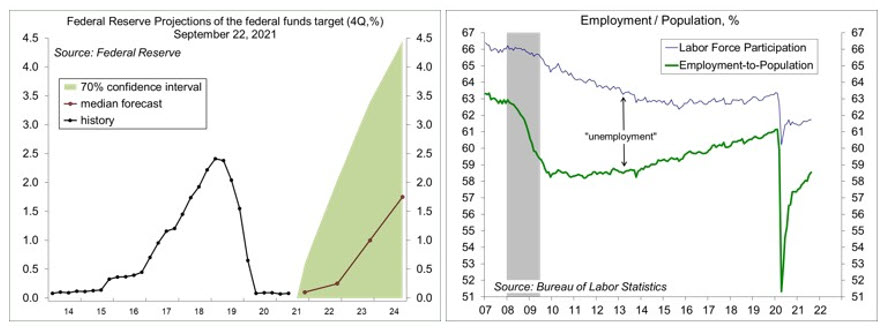

The dot plot shows senior Fed officials’ expectation of the appropriate federal funds target rate at the end of each of the next few years. No surprise, many of the dots shifted higher. In his press conference, Powell noted that the dots “do not represent a Committee decision of plan, and no one knows where the economy will be a couple of years from now.” Indeed, within the SEP, the Fed discussed the “considerable” uncertainty in its forecasts, including the outlook for short-term interest rates.

There is always uncertainty in economic forecasts, but that uncertainty is much higher than usual given the nature of the pandemic. Some pandemic-related changes in economic behavior are likely to be longer lasting, such as the shift from consumer services to goods. Some may be permanent, such as working from home. A key uncertainty is labor force participation. Childcare issues and fear of the virus have kept some potential workers out of the labor force. Older workers who opted for early retirement are unlikely to return. Anecdotal information suggests that many of those in low skilled positions have been reluctant to return. A scarcity of labor should lead (eventually) to a reallocation of workers to more productive endeavors and those on the sidelines may return to the labor force, but that takes time. In the short term, many industries have reported forgoing increased production due to a lack of skilled labor, which adds to inflation pressure.

The evolution of the labor market will be a key element in the outlook for Fed policy. Low income workers were hardest hit during the pandemic and will be the last to recover. Some of the difficulties will take time to resolve, which means that the Fed should remain accommodative. If these difficulties persist, then the Fed may face some tough choices in the quarters ahead.

The FOMC Decision and Summary of Economic Projections

As expected, the Federal Open Market Committee left short-term interest rates unchanged and did not alter the monthly pace of asset purchases. The FOMC indicated that “if progress continues broadly as expected, the Committee judges that a moderation in the pace of asset purchases may soon be warranted.” Chair Powell said that the goal of “substantial further progress” in labor market conditions would likely be met in the October Employment Report, which would lead to a taper announcement at the November 2-3 policy meeting.

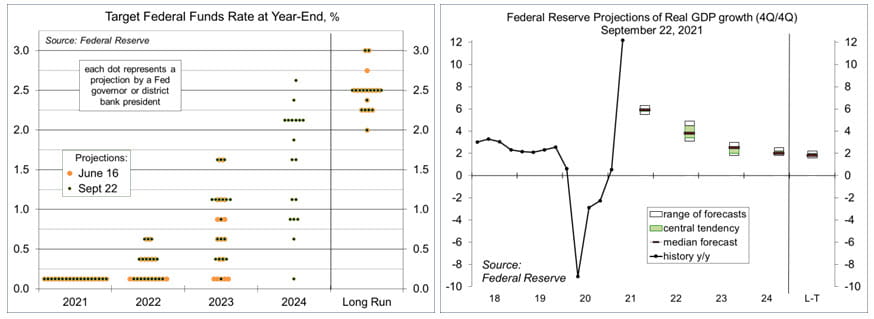

The revised dot plot (which is a general expectation and not a plan) showed that senior Fed officials were evenly split on expectations of whether it would be appropriate to raise short-term interest rates in 2022.

The median projection of real GDP growth for this year fell to 5.9% (4Q21/4Q20), down from 7.0% in June and 6.5% in March. That works out to a 5.4% annual rate in the second half of this year (vs. +6.4% in the first half of the year). While there was a wide range of expectations for 2022 GDP growth (3.0% to 4.0%), the median forecast rose to 3.8% (from 3.3% in June).

Fed officials further raised their projections of 2021 inflation (median: 4.2%, vs. 3.4% in June, 2.4% in March, and 1.8% last December), but still expect inflation to fall back toward the long-term 2% goal (a median forecast of 2.2% in both 2022 and 2023).

Fed officials generally expect the unemployment rate to fall a bit less this year (median forecast for 4Q21: 4.8%, vs. 4.5% in June).

Recent Economic Data

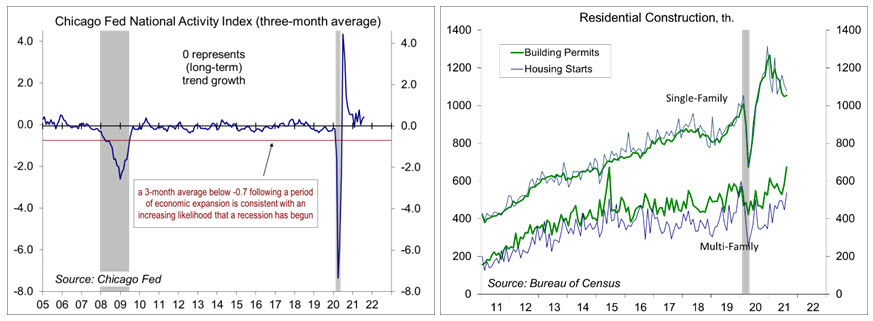

The Chicago Fed National Activity Index, a composite of 85 economic indicators, fell to 0.29 in August, down from 0.75 in July (the index is scaled to have a mean of 0 and a standard deviation of 1). The three-month average was 0.43, consistent with slower, but still above-average growth.

Single-family building permits rose 0.6% in August, virtually unchanged (-0.1%) from a year ago. Total permits jumped 6.0% (+13.5% y/y), reflecting a surge in multi-family activity (which tends to be volatile. Housing starts rose 3.9% (+17.4% y/y), although single-family starts were reported down 2.8% (+5.2% y/y).

Existing home sales fell 2.0% in August, to a 5.88 million seasonally adjusted annual rate (-1.5% y/y).

New home sales rose 1.5% (±15.1%) in August, to a 740,000 seasonally adjusted annual rate, with mixed results across regions. Sales were down 24.3% from a year ago, but appear near to the pre-pandemic trend.

The Conference Board’s Index of Leading Economic Indicators rose 0.9% in August, consistent with continued economic expansion in the near term (but the LEI tells us nothing about the strength).

The Current Account deficit was little changed in 2Q21 ($190.3 billion, vs. $189.4 billion in 1Q21), which is about 3.3% of GDP (vs. 1.9% of GDP in 4Q19).

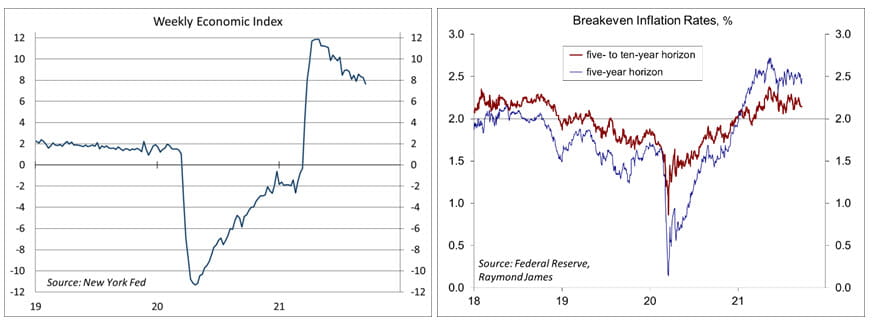

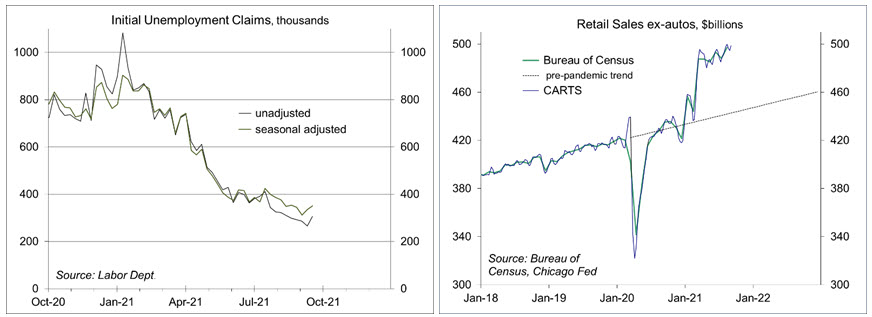

Gauging the Recovery

The New York Fed’s Weekly Economic Index fell to +7.64% for the week ending September 18, vs. +8.25% a week earlier (revised from +7.84%). The WEI is scaled to y/y GDP growth (- 2.9% y/y in 3Q20).

Breakeven inflation rates (the spread between inflation-adjusted and fixed-rate Treasuries, not quite the same as inflation expectations, but close enough) continue to suggest a moderately higher near-term inflation outlook. The 5- to 10-year outlook remains consistent with the Fed’s long-term goal of 2%.

Jobless claims rose by 16,000, to 351,000 in the week ending September 18, reflecting a large increase (+24,000) in claims in California. The end of extended benefits (Labor Day, although many states had pulled back on federal assistance before that) should coincide with a decrease in claims, but seasonal adjustment is large and weekly figures are often noisy in September.

Chicago Fed Advance Retail Trade Summary (CARTS): the Weekly Index of Retail Trade increased 0.8% on a seasonally adjusted basis after decreasing 0.3% in the previous week. September retail sales (ex-autos) were projected to rise 0.6% from August.

The University of Michigan’s Consumer Sentiment Index fell to 70.3 in the mid-month assessment for September (the survey covered August 25 to September 15), vs. 70.3 in July and 81.2 in July. Expectations edged up to 67.1 (it sank from 79.0 in July to 65.1 in August).

The opinions offered by Dr. Brown are provided as of the date above and subject to change. For more information about this report – to discuss how this outlook may affect your personal situation and/or to learn how this insight may be incorporated into your investment strategy – please contact your financial advisor or use the convenient Office Locator to find our office(s) nearest you today.

This material is being provided for informational purposes only. Any information should not be deemed a recommendation to buy, hold or sell any security. Certain information has been obtained from third-party sources we consider reliable, but we do not guarantee that such information is accurate or complete. This report is not a complete description of the securities, markets, or developments referred to in this material and does not include all available data necessary for making an investment decision. Prior to making an investment decision, please consult with your financial advisor about your individual situation. Investing involves risk and you may incur a profit or loss regardless of strategy selected. There is no guarantee that the statements, opinions or forecasts provided herein will prove to be correct.

Markets & Investing Members of the Raymond James Investment Strategy Committee share their views on...

Markets & Investing Review the latest Weekly Headings by CIO Larry Adam. Key Takeaways ...

Technology & Innovation Learn about a few simple things you can do to protect your personal information...