Chief Economist Scott Brown discusses current economic conditions.

The Bureau of Labor Statistics reports that all 50 states experienced a decrease in payrolls and an increase in unemployment in April. Following some weeks of varying degrees of mandated social distancing, all 50 states have now begun to open up their economies. The near-term economic data are expected to reflect a sharp contraction in 2Q20. The outlook is uncertain, but appears likely to disappoint relative to earlier hopes of a rapid rebound.

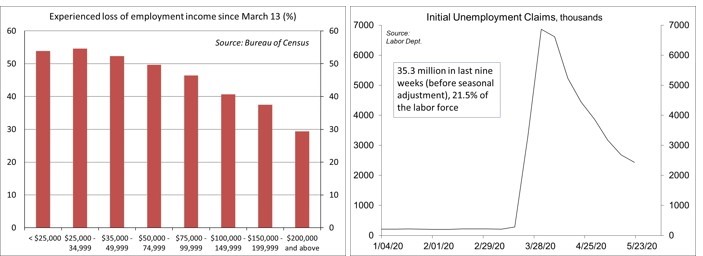

The Bureau of Census has recently released results of a couple of experimental surveys to gauge the real-time economic effects of the coronavirus and the efforts to contain it: a Small Business Pulse Survey and a Household Pulse Survey. Each has a set of tables and an interactive feature which allows comparisons across states and industries. These figures will be updated every Thursday. The Household Pulse Survey confirms what was already suggested by the anecdotal information. All income sectors have experienced a loss of labor income through this crisis, with lower- income households experiencing the worst.

Weekly jobless claims fell further in the week ending May 16, but the level remains extremely elevated. Investors have begun to turn their attention to continuing claims, which are reported with a lag. Continuing claims can be hard to interpret. A decline could signal job growth, but it can also signal an exhaustion of benefits. Claims were still rising in the week ending May 9, to over 25 million. Extended benefits are set to expire at the end of July. It’s unlikely that we’ll see a huge surge in job offerings through the end of the year.

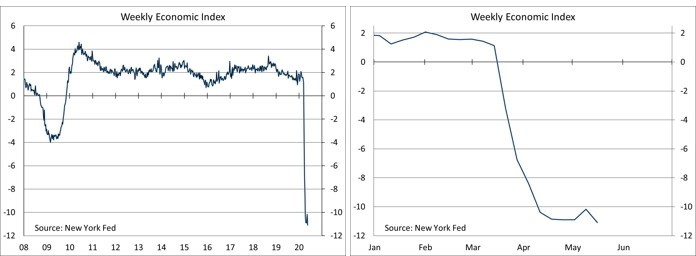

The New York Fed has unveiled a Weekly Economic Index, updated on Tuesdays and Thursdays, created by Daniel Lewis (of the NY Fed), Karel Mertens (of the Dallas Fed), and James Stock (of Harvard – having Stock on board is effectively the econometrician’s Seal of Approval). The WEI is a composite index of ten real-time indicators, many of which are proprietary. It is scaled to correspond to GDP growth. For example, the current reading, at -11.09, means that GDP would fall 11.09% if sustained for four quarters. The sharp drop since early March signals that the current downturn is much worse than what we saw through the financial crisis. More recently, the data suggest that the economy could be in the process of bottoming. The WEI will bear close watching in the weeks ahead.

There are a couple of important data issues for investors to consider. One is that U.S. GDP growth is reported at an annual rate, which exaggerates the quarterly change. For example, if GDP were to contract 10% in a single quarter, it would be reported as a -34% annual rate (as if that 10% quarterly decline had continued for four quarters). As the economy begins to recover, data reports may be difficult for investors to interpret. GDP growth is expected to rise sharply in 3Q20, but not enough to make up for the ground lost in the second quarter.

The nonpartisan Congressional Budget Office has a good track record in forecasting the economy. That doesn’t mean the CBO is always right, but projections tend to be close to the general expectation of private-sector economists. There’s nothing to suggest a pattern of “wishful thinking.” The CBO’s recent updated outlook shows a sharp departure from what was anticipated in January. The CBO now expects the economy to contract at a 37.7% annual rate in 2Q20. GDP is projected to rebound at a 21.5% annual rate in 3Q20, which would be the strongest quarter ever. Is that good? Not from the perspective of where we were before the pandemic.

The CBO’s outlook is not far from what most economists are anticipating, but there’s a lot of uncertainty. The key features are the depth of the decline and the gap between the recovery path and the prior trend. The drop could be steeper or not as steep. The rebound could be faster or slower. We could find the level of GDP far below trend in late 2021. However, the general pattern (sharp decline, gradual recovery) seems the most likely result.

The longer-term outlook has worsened in recent weeks. Temporary job losses have a way of becoming permanent. Concerns about the immediate loss of jobs related to social distancing are giving way to worries about second- and third-round effects (the loss of income hitting consumer spending and increasing strains in state and local government budgets). Credit market fears about liquidity, well met by an aggressive response from the Federal Reserve, are shifting to issues of solvency. Consumer spending should bounce off of the lows as the states open up, but many people will be reluctant to travel, to stay in a hotel, to go to a restaurant or sporting event, or to go shopping. Many have feared that we’ll see a second wave of infections if the economy opens too fast. Rather, we are more likely to see a moderately high rate of infections (and deaths), with a mixed level of self-imposed social distancing. Investors should look to the real-time economic data with some degree of optimism, but continue to keep an eye on the coronavirus figures. (M20-3098810)

The opinions offered by Dr. Brown should be considered a part of your overall decision-making process. For more information about this report – to discuss how this outlook may affect your personal situation and/or to learn how this insight may be incorporated into your investment strategy – please contact your financial advisor or use the convenient Office Locator to find our office(s) nearest you today.

All expressions of opinion reflect the judgment of the Research Department of Raymond James & Associates (RJA) at this date and are subject to change. Information has been obtained from sources considered reliable, but we do not guarantee that the foregoing report is accurate or complete. Other departments of RJA may have information which is not available to the Research Department about companies mentioned in this report. RJA or its affiliates may execute transactions in the securities mentioned in this report which may not be consistent with the report’s conclusions. RJA may perform investment banking or other services for, or solicit investment banking business from, any company mentioned in this report. For institutional clients of the European Economic Area (EEA): This document (and any attachments or exhibits hereto) is intended only for EEA Institutional Clients or others to whom it may lawfully be submitted. There is no assurance that any of the trends mentioned will continue in the future. Past performance is not indicative of future results.

Markets & Investing Members of the Raymond James Investment Strategy Committee share their views on...

Markets & Investing Review the latest Weekly Headings by CIO Larry Adam. Key Takeaways ...

Technology & Innovation Learn about a few simple things you can do to protect your personal information...