Chief Economist Scott Brown discusses current economic conditions.

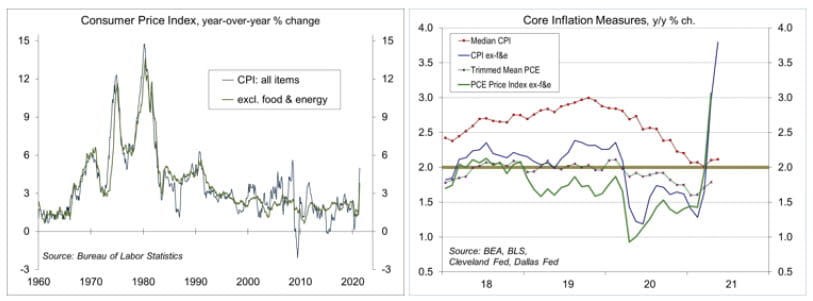

Oh, wow, déjà vu. Once again, the monthly increase in the CPI exceeded expectations. The Consumer Price Index has now posted its largest two-month increase, and its largest year-over-year increase, since mid-2008. So, naturally, bond yields are… lower???

The CPI rose 0.6% in May, up 5.0% y/y. As with the increase in April, there were three factors. Base effects (a rebound from low levels of a year ago) are about at their maximum. The CPI was up 0.1% y/y in May 2020. Half of the May increase in the CPI was related to vehicles: prices of new cars, used cars, car insurance, and car rentals. The lockdowns of a year ago reduced the number of vehicles going to rental agencies. As a result, there is reduced supply into the used car market this year, while there is an increased demand for vehicles as the economy opens up. This imbalance won’t last forever. Prices in transportation services, including airfares and all the car stuff, were down a year ago. A recovery in these prices is transitory.

Ex-food and energy, the CPI rose 0.7% (+3.8% y/y), following a 0.9% increase in April. It was the largest two-month increase since 1982 (and the largest y/y increase since 1992). There are other measures of core inflation (the ex-food & energy figures is the most common). The Cleveland Fed’s median CPI, which calculates the middle of the range of component price increases, rose 0.3% in May, up just 2.1% y/y. The Dallas Fed’s Trimmed- Mean PCE Price Index had also signaled low y/y inflation in April. The increase in inflation is not broad-based.

Commodity price pressures are notable in every economic recovery, reflecting bottleneck production pressures and materials shortages. These pressures fade as the economy recovers. In the current environment, these pressures have been more intense, reflecting the rapid improvement in the economy. However, prices of copper and many other industrial inputs have started to decline. Demand for commodities should remain strong as the global economy improves, but the global outlook is mixed and it will be some time before we see a full worldwide recovery.

Base effects and restart pressures fall into the transitory category, but there are other concerns. Labor market frictions ought to put upward pressure on wages. Workers who didn’t get a raise because of the pandemic will expect to make up the difference as we head into 2022, but they may not wait that long. Quit rates rose to a record high in April (the Bureau of Labor Statistics data only goes back to December 2000). The other issue is inflation expectations. Consumer surveys and market-based measures of inflation expectations picked up last month, but they have already begun to moderate in early June.

The tide has turned in the inflation debate among investors, and we are likely to see a further retreat in inflation fears following the June 15-16 Fed policy meeting. While there has been some internal debate about inflation among Fed policymakers, there is more evidence supporting the view that the recent increase in inflation will prove to be transitory.

Recent Economic Data

The Consumer Price Index rose 0.6% in May (+5.0% y/y, vs. +0.1% y/y in May 2020), up 0.7% ex-food & energy (+3.8% y/y, vs. +1.2% in May 2020). The increase was more than expected, although continued to reflect base effects (a rebound from the low levels of a year ago), restart pressures, and another pop in the price of used vehicles (+7.3%, following +10.0% in April). Half of the May increase in the headline CPI was in prices of new vehicles, used vehicles, car insurance, and vehicle rentals.

The U.S. trade deficit fell to $68.9 billion in April, down from a record $75.0 billion in March (up from $53.0 billion in April 2020). Exports rose 1.1% (+36.6% y/y), while imports fell 1.4% (+34.9% y/y).

The Job Opening and Labor Turnover Survey (JOLTS) results for April showed a record number of job openings in April (9.29 million overall, 8.37 million for the private sector).

The Federal Reserve’s Z.1 Financial Accounts Report showed household wealth rising to $136.9 trillion in 1Q21, up 3.8% from 4Q20 and 16.2% higher than before the pandemic.

Gauging the Recovery

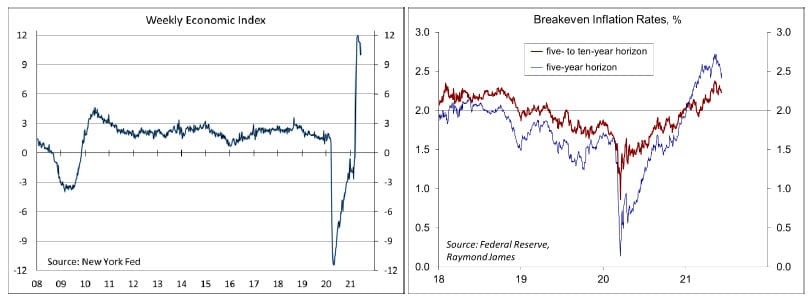

The New York Fed’s Weekly Economic Index edged down to +10.01% for the week ending June 5, vs. +11.24% a week earlier (revised from +10.79%), signifying strength relative to the depressed level of a year ago. The WEI is scaled to year-over-year GDP growth (GDP was down 9.0% y/y in 2Q20).

Breakeven inflation rates (the spread between inflation-adjusted and fixed-rate Treasuries, not quite the same as inflation expectations, but close enough) continues to suggest a moderately higher near-term inflation outlook. The 5-10-year outlook had crept above the Fed’s long-term goal of 2%, but has moderated.

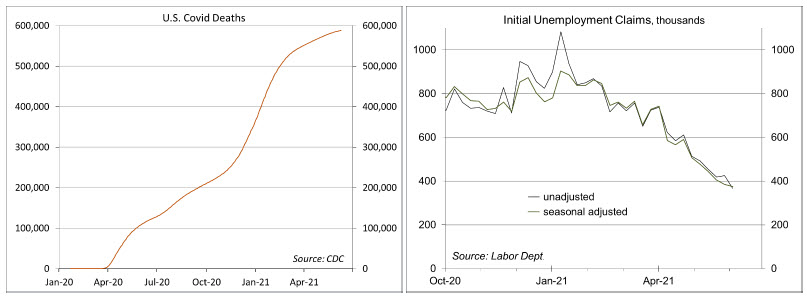

As more people become vaccinated, the number of COVID-19 cases continues to trend lower. Despite the downtrend in new cases, we are still losing about 2,400 people per week (vs. 4,000 at the end of April).

Jobless claims fell by 9,000, to 376,000 (another pandemic low), in the week ending June 5. Seasonal adjustment around the holiday adds uncertainty, but the trend is clearly lower.

The University of Michigan’s Consumer Sentiment Index rebounded to 86.4 in the mid-month assessment for June (the survey covered May 26 to June 9), vs. 82.9 in May and 88.3 in April. The increase was concentrated among mid- and upper-income household, reflecting greater optimism as the economy re-opens. Inflation concerns remained, but less than in May.

The opinions offered by Dr. Brown are provided as of the date above and subject to change. For more information about this report – to discuss how this outlook may affect your personal situation and/or to learn how this insight may be incorporated into your investment strategy – please contact your financial advisor or use the convenient Office Locator to find our office(s) nearest you today.

This material is being provided for informational purposes only. Any information should not be deemed a recommendation to buy, hold or sell any security. Certain information has been obtained from third-party sources we consider reliable, but we do not guarantee that such information is accurate or complete. This report is not a complete description of the securities, markets, or developments referred to in this material and does not include all available data necessary for making an investment decision. Prior to making an investment decision, please consult with your financial advisor about your individual situation. Investing involves risk and you may incur a profit or loss regardless of strategy selected. There is no guarantee that the statements, opinions or forecasts provided herein will prove to be correct.

Markets & Investing Members of the Raymond James Investment Strategy Committee share their views on...

Markets & Investing Review the latest Weekly Headings by CIO Larry Adam. Key Takeaways ...

Technology & Innovation Learn about a few simple things you can do to protect your personal information...