Chief Economist Scott Brown discusses current economic conditions.

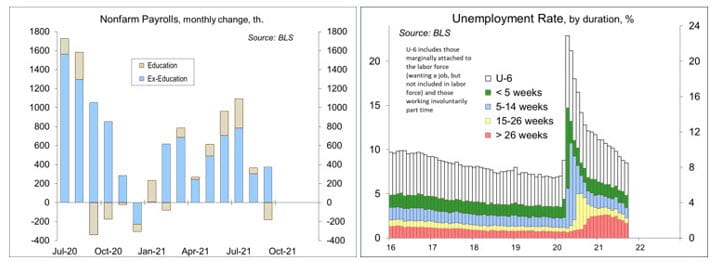

There was another “disappointing” gain in nonfarm payrolls in September (up 194,000, vs. a median forecast of +500,000), but it’s not as bad as it looks. Less hiring at the start of the school year resulted in a decline in (adjusted) education jobs. Non- education jobs rose by 374,000 (with a three-month average of +487,000). As Fed Chair Powell indicated in his September 22 press conference, the central bank is not going to base its tapering decision on any one report, but this release adds to evidence of “substantial further progress” in labor market conditions (the taper trigger). There is some debate about how much slack remains in the job market, but no chance that the Fed will raise short-term interest rates anytime soon.

There are seasonal patterns in the job market. The holiday shopping period is a major one. Another is the school year. We normally add about 1.5 million education jobs each September (and another 650,000 or so in October). This September, we added 1.3 million. Seasonal adjustment turns that into a decline of 180,000 in adjusted education jobs. We saw this play out in the previous school year, where less hiring at the start led to fewer layoffs at the end, which translated into large (adjusted) education “gains” in June and July. The Delta variant was surely a constraint on job growth last month, in which case we should see a pickup as new COVID cases decline. We also saw an upward revision of 169,000 to July and August.

While the payroll gain was lower than expected, the drop in the unemployment rate (to 4.8%, from 5.2%) was a bigger surprise. Some of that was due to the end of extended unemployment benefits. Instead of boosting employment, the expiration of extended benefits led some to drop out of the labor force. In most cases, to receive unemployment benefits, one has to be actively looking for a job, which also satisfies the definition of “unemployed” (without a job, but actively looking). If you give up looking, as many do when benefits expire, you are no longer classified as “unemployed.” Labor force participation did edge down last month (to 61.6%, from 61.7%), still well below the pre-pandemic level (63.3%).

So how much slack is there in the job market? Outside surveys, if you can believe them, suggest that about 30% of restaurant workers and other low-wage employees are reluctant to go back to their old jobs. We’ve cut legal immigration and baby-boomers are retiring in a “gray wave.” So, we may start to worry about the growth in the labor force within the next few years. In the meantime, nonfarm payrolls remain down about 5 million from before the pandemic and we would have added about 3.1 million jobs over the last 19 months if not for the pandemic. That’s a lot of slack, but businesses continue to report difficulties finding workers. That likely reflects skill and locational mismatches, which ought to clear up over time, but could persist.

For Fed policymakers, there’s nothing in the September Employment Report that would prevent a taper announcement in November. The showdowns over the budget and federal debt ceiling have been put off to December. Political uncertainty could be a factor in delaying the Fed’s taper decision, but that may depend on whether political uncertainty translates into financial market turmoil.

Recent Economic Data

The ISM Services Index edged up to 61.1 in September, vs. 59.9 in August and 59.5 in July. The report showed continued strength in new orders and production, but continued strains in supply chains.

Nonfarm payrolls rose by 194,000 in the initial estimate for September, held down by reduced hiring at the start of the school year (which resulted in a 180,000 decline in adjusted education jobs). Payrolls remain about 5 million lower than before the pandemic, but we would probably added 3.1 million jobs if not for the pandemic.

The unemployment rate fell to 4.8%, partly reflecting a drop in labor force participation (related to the end of extended unemployment benefits). The employment/population ratio rose to 58.7%, up from 58.5% in August and 56.6% a year ago, but well below the pre-pandemic level of 61.1%.

Unit motor vehicle sales fell 6.4% to a 12.2 million seasonally adjusted annual rate in September, down 33.4% since April. The drop reflects the semiconductor shortage’s impact on production, not weak demand.

The U.S. trade deficit widened to a record $73.3 trillion in August. Merchandise exports rose 0.7% (+25.8% y/y), while imports rose 1.1% (+18.4% y/y). The surplus in services fell to $16.2 billion, the lowest since 2011.

Factory orders rose 1.2% in August, reflecting a 77.9% jump in civilian aircraft orders. Ex-transportation, orders rose 0.5%, mixed across industries. Orders for nondefense capital goods ex-aircraft rose 0.6%

Gauging the Recovery

The New York Fed’s Weekly Economic Index fell to +7.78% for the week ending October 2, vs. +8.02% a week earlier (revised from +7.58%). The WEI is scaled to y/y GDP growth (- 2.9% y/y in 3Q20). A year ago, the index stood at -4.73%.

Breakeven inflation rates (the spread between inflation-adjusted and fixed-rate Treasuries, not quite the same as inflation expectations, but close enough) continue to suggest a moderately higher near-term inflation outlook. The 5- to 10-year outlook remains consistent with the Fed’s long-term goal of 2%.

Jobless claims fell by 38,000, to 326,000 in the week ending October 2, partly reflecting a drop in claims in California (which had been elevated in the two previous weeks). The end of extended benefits has led to a sharp drop in total claimants in recent weeks (to 4.2 million, from 11.3 million).

Chicago Fed Advance Retail Trade Summary (CARTS): the Weekly Index of Retail Trade increased 0.8% on a seasonally adjusted basis after decreasing 0.3% in the previous week. September retail sales (ex-autos) were projected to rise 0.6% from August.

The University of Michigan’s Consumer Sentiment Index edged up to 72.8 in the full-month assessment for September (the survey covered August 25 to September 27), vs. 71.0 at mid-month and 70.3 in July. The report noted a “depressed optimism” sparked by the Delta variant. Inflation psychology does not appear rooted, but consumers generally expect reduced income gains after adjusting for inflation.

The opinions offered by Dr. Brown are provided as of the date above and subject to change. For more information about this report – to discuss how this outlook may affect your personal situation and/or to learn how this insight may be incorporated into your investment strategy – please contact your financial advisor or use the convenient Office Locator to find our office(s) nearest you today.

This material is being provided for informational purposes only. Any information should not be deemed a recommendation to buy, hold or sell any security. Certain information has been obtained from third-party sources we consider reliable, but we do not guarantee that such information is accurate or complete. This report is not a complete description of the securities, markets, or developments referred to in this material and does not include all available data necessary for making an investment decision. Prior to making an investment decision, please consult with your financial advisor about your individual situation. Investing involves risk and you may incur a profit or loss regardless of strategy selected. There is no guarantee that the statements, opinions or forecasts provided herein will prove to be correct.

Markets & Investing Members of the Raymond James Investment Strategy Committee share their views on...

Markets & Investing Review the latest Weekly Headings by CIO Larry Adam. Key Takeaways ...

Technology & Innovation Learn about a few simple things you can do to protect your personal information...