April 5, 2021

Chief Economist Scott Brown discusses current economic conditions.

As the pandemic recedes and the economy reopens, we can expect strong job growth in the months ahead. The March figures were a start. We may soon see monthly gains in nonfarm payrolls of a million or more. However, as employment rebounds, labor market frictions are more likely to come into play, reflecting the scarring that has occurred over the last several months. It is unclear how much of this will lead to higher wage and price inflation, but pressures ought to be transitory.

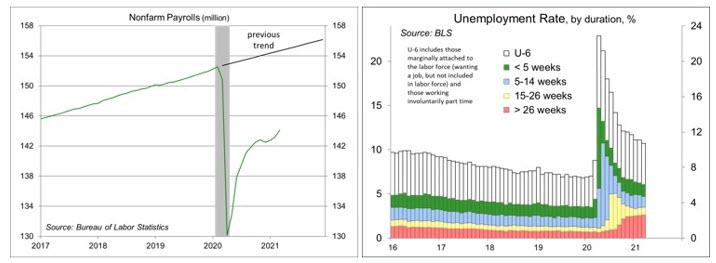

Prior to seasonal adjustment, the economy added 1.3 million jobs last month, or 917,000 after adjustment. Spring is the strongest part of the year for (unadjusted) job growth. Prior to the pandemic, unadjusted payrolls would normally rise by 3.2 million or more between February and June. So clearly, payrolls can expand rapidly without much trouble. Currently, payrolls are about 9 million below the pre-pandemic level and about 11 million below the previous trend (as if the pandemic had not occurred).

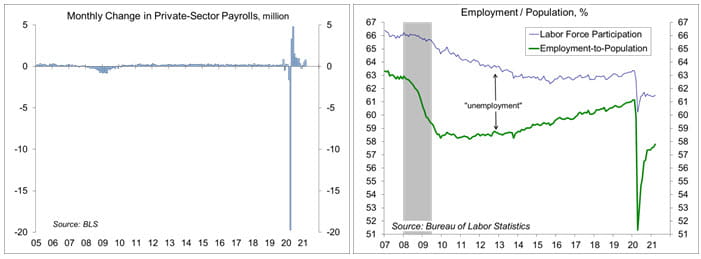

The unemployment rate fell to 6.0% in March, but this is a misleading figure, as labor force participation remains well below pre-pandemic levels (61.5%, vs. 63.4%). In addition, there are more than 5.8 million people working part time who would rather have full-time employment. The broad U-6 measure of unemployment, which includes discouraged workers and others marginally attached to the labor force plus those involuntarily working part time, was 10.7% in March. Looking more broadly at the unemployment situation, some workers have been without work throughout the pandemic, some in the industries less directly hit have been let go along the way, and some have moved into and out of short-term employment.

One of the fears early in the pandemic was the issue of scarring. This refers to the destruction of relationships: between firms and workers; between lenders and borrowers; and between sellers and buyers. Scarring gets worse the longer the downturn lasts and is usually a lot worse when the cause of the downturn is a financial crisis. Many small businesses may not exist anymore. Many of the unemployed may not have a job to which they can return. A manufacturer looking for parts may have to struggle for alternatives if a key supplier is no longer in business. Firms may have a hard time locating skilled workers who were furloughed months earlier.

Fortunately, the pandemic did not result in significantly weaker financial conditions. Thanks to aggressive monetary and fiscal policies, there was no chain reaction of financial contagion. That’s not to overlook the real damage to the economy, businesses, and households. Rather, it could really have been a lot worse.

Matching unemployed workers to available jobs could be difficult, especially when skill, education, or experience are required. This could lead to added wage pressures in some sectors. However, much of the pandemic-related weakness has been in lower-skilled service industries, which should be easier to refill, and this I where we expect to see the biggest job gains. Still, while the job outlook is optimistic, the overall level of uncertainty in the economic outlook is high.

Recent Economic Data

Nonfarm payrolls rose by 916,000 in March, down about 11 million from the prior trend.

The unemployment rate fell to 6.0% in March, but that understates the weakness in the labor market. The employment/population ratio was 57.8%, vs. 61.1% before the pandemic.

The Conference Board’s Consumer Confidence Index rose to 109.7 in the initial estimate for March, up from

90.4 in February. The index was 132.6 in February 2020 and hit a low of 85.7 in April 2020.

The ISM Manufacturing Index rose to 64.7 in March, following 60.8 in February. Comments from supply managers noted “extended lead times, wide-scale shortages of critical basic materials, rising commodities prices and difficulties in transporting products are affecting all segments of the manufacturing economy.” The Chicago Business Barometer rose to 66.3 in March, up from 59.5 in February.

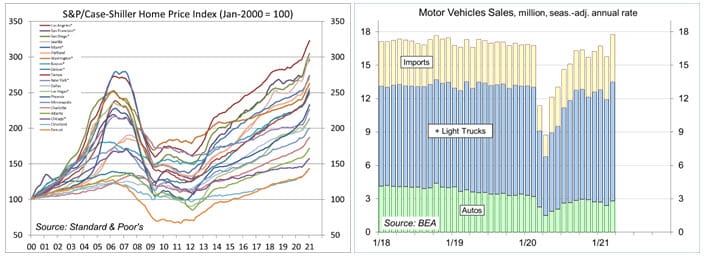

The Case Shiller Home Price Index rose 1.2% in January, up 11.2%. Of the 20 metropolitan areas covered, 15 had year-over-year increase more than 10%.

Unit motor vehicle sales rose to a 17.7 million seasonally adjusted annual rate in March, up from 15.8 million in February and 16.7 million in January – the strongest since October 2017.

The Pending Home Sales Index fell 10.6% in February (-0.5%), partly reflecting bad weather, but a lack of available homes for sale appeared to be the main drawback.

Gauging the Recovery

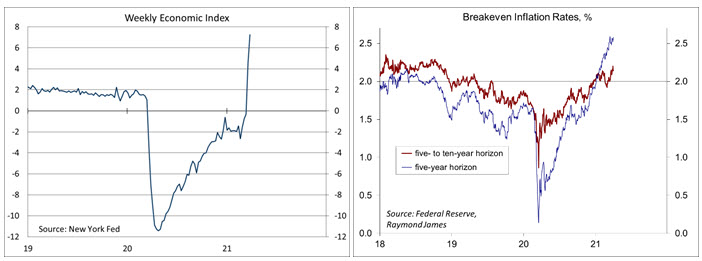

The New York Fed’s Weekly Economic Index rose to +7.25% for the week ending March 27, up from +4.51% a week earlier (revised from +4.14%), signifying strength relative to the weak data of a year ago. The WEI is scaled to year-over-year GDP growth (we should see it rising further in the weeks ahead).

Breakeven inflation rates (the difference between inflation-adjusted and fixed-rate Treasuries) continue to suggest a moderately higher inflation outlook for the next five years, but the outlook five to ten years out remains close to the Fed’s long-term goal of 2% (consistent with the Fed’s revised monetary policy framework).

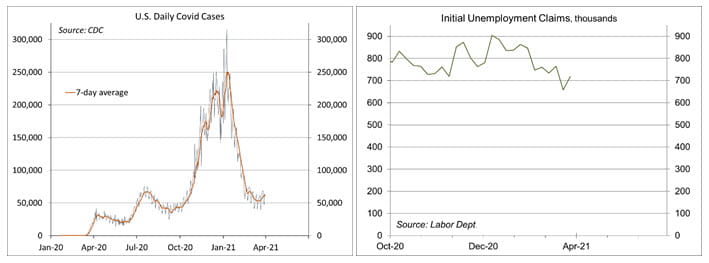

The trend in COVID-19 cases has started to turn up, raising concerns about a possible fourth wave.

Jobless claims rose by 61,000, to 719,000, in the week ending March 27 (714,333 before seasonal adjustment). Figures have been uneven in recent weeks, but the overall trend is moderately lower. The continued elevated level of claims appears to reflect people repeatedly getting short-term work.

The University of Michigan’s Consumer Sentiment Index rose to 84.9 (a 12-month high) in the full-month assessment for March (the survey covered February 24 to March 22), vs. 83.0 at mid-month and 76.8 in February. The report noted gains from disbursement of relief checks and better than anticipated vaccination progress. The data point toward “robust increases in consumer spending.”

The opinions offered by Dr. Brown are provided as of the date above and subject to change. For more information about this report – to discuss how this outlook may affect your personal situation and/or to learn how this insight may be incorporated into your investment strategy – please contact your financial advisor or use the convenient Office Locator to find our office(s) nearest you today.

This material is being provided for informational purposes only. Any information should not be deemed a recommendation to buy, hold or sell any security. Certain information has been obtained from third-party sources we consider reliable, but we do not guarantee that such information is accurate or complete. This report is not a complete description of the securities, markets, or developments referred to in this material and does not include all available data necessary for making an investment decision. Prior to making an investment decision, please consult with your financial advisor about your individual situation. Investing involves risk and you may incur a profit or loss regardless of strategy selected. There is no guarantee that the statements, opinions or forecasts provided herein will prove to be correct.

Markets & Investing Members of the Raymond James Investment Strategy Committee share their views on...

Markets & Investing Review the latest Weekly Headings by CIO Larry Adam. Key Takeaways ...

Technology & Innovation Learn about a few simple things you can do to protect your personal information...